The feeling from high interest levels to your mortgage repayments

Addition

Because the , interest levels has actually risen considerably and quickly following a time period of historic reasonable prices inside first couple of years of new COVID?19 pandemic. Thus, of many financial proprietors are presently against notably high repayments, and others will perform so within revival. The specific sized it boost in costs depends on the brand new top features of for each and every mortgage and exactly how rates continue steadily to evolve.

To evaluate exactly how rates of interest you may next impact the price of upkeep mortgages, i explore loan-height analysis to help you simulate upcoming mortgage payments according to the expectation you to definitely interest levels progress predicated on monetary sector standards.step 1 For this reason, which simulation was hypothetical and will not represent a prediction.

- Towards the end away from , regarding forty five% of one’s mortgage loans applied for until the Bank regarding Canada started increasing their plan rate of interest inside the got seen a boost in repayments. By the end out-of 2026, nearly all remaining mortgage people within group goes owing to a revival period and you may, with respect to the roadway to own interest levels, may deal with significantly higher repayments.

- Consumers who either got away home financing during the 2021-when rates was indeed in the historic downs-otherwise opted for an adjustable financial rates will generally have seen the largest increases when you look at the repayments towards the end from 2026. Among varying-price financial proprietors, people who have repaired repayments who’ve perhaps not drawn action to cease highest future grows could well be impacted on revival. For it category, average repayments are needed to increase from the 54% during the months within stop away from , ahead of rates started to raise, additionally the prevent of 2027. However, people with changeable money have been inspired, having average repayments upwards 70% inside the compared with its level at the conclusion of . But not, centered on sector rate requirement, money are essential in order to .

- The latest effect off high rates of interest into borrowers’ power to shell out their financial usually mostly believe the future money. Without any income development, the median debtor could need to purchase around 4% a lot more of their pre-tax earnings so you can mortgage payments towards the end regarding 2027. not, for the majority consumers, income gains you’ll mitigate new impact away from highest interest rates towards personal debt serviceability.

It is important to keep in mind that our simulation does not account having possible alterations in new conduct of individuals, such as and work out expidited repayments or using a unique financial unit. Including changes create help protect against (although not stop) the rise in the money. Hence, the simulation performance represent a top-bound guess.

The new dataset

The simulator uses anonymized, regulating, loan-height study collected of the Work environment of your own Superintendent off Financial Associations (OSFI), Canada’s financial regulator. Microdata compiled by OSFI have the very complete pointers Northford loans accessible to get acquainted with the fresh impression interesting prices to your mortgage payments during the Canada, enabling more exact and you can granular simulation it is possible to. Regarding the dataset employed for this new simulator, i observe for every single mortgage from the origination (having both a new buy otherwise a mortgage re-finance) at renewal. The brand new dataset boasts regarding sixteen million mortgage findings just like the 2014. Several extremely important cards about this dataset:

- It includes home loan interest during the federally regulated lenders, for instance the Larger Half a dozen Canadian banks and shorter finance companies. Mortgages in the other sorts of lenders, like credit unions and you can mortgage resource people (MFCs), aren’t one of them dataset since these loan providers are maybe not controlled by OSFI.dos Our dataset hence talks about throughout the 80% of your own full home loan markets.

- They grabs various loan and you will debtor features, such as the:3

- initial (contractual) interest

- earnings used in the application to be eligible for the mortgage

- size of the borrowed funds

- contractual amortization period

The newest simulator do it

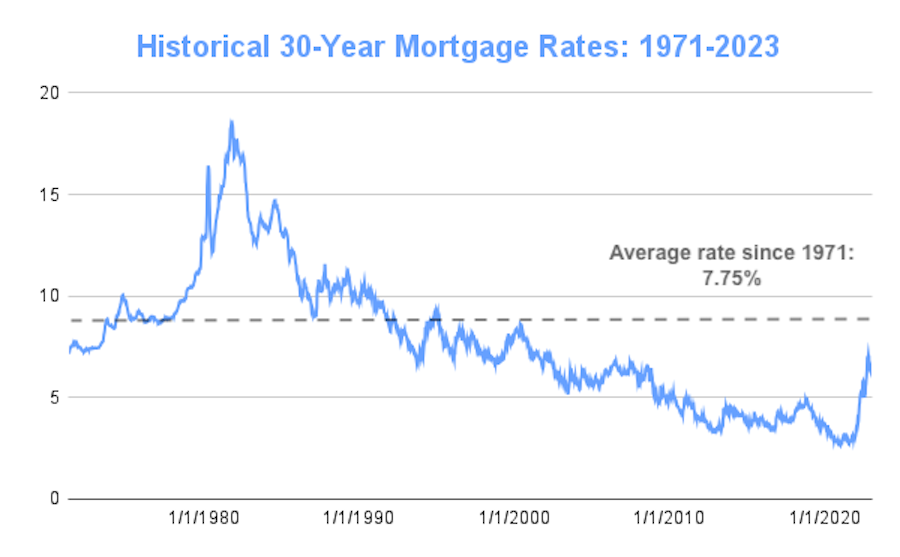

Per home loan within dataset, i assess the loan fee over background immediately after which imitate the fresh new future repayments predicated on a believed path to possess rates. We construct the pace path playing with historic financial prices joint with standard produced by monetary locations for both the coverage appeal price and you will authorities bond costs. Since the revealed into the Chart 1, in mid-, monetary locations were pregnant the policy interest rate so you’re able to height at the the conclusion 2023 after which continue to be higher than it had been typically over the years up until the pandemic. We use the path once the a benchmark to your speed increase each person home loan will face.six